1. Introduction

From March 2023 to March 2024, there have been 31 reported arson incidents across urban and rural Victoria, at retail outlets selling tobacco products (Hevesi, 2024). While a ‘turf war’ between crime family–based syndicates (Epstein, 2024) or motorcycle gangs (Collins, 2023) is suspected, the situation escalated in October 2023 with the first suspected death of a person ‘linked’ to the illicit tobacco trade who was shot by four assailants in a suburban Melbourne shopping centre (Collins, 2023; Lantouris, 2023).

The most common analysis of the illicit tobacco market has been the loss of government revenue, in particular excise taxes, which represent the major form of taxation falling on tobacco products. In Australia, at the time of writing, the excise tax rate on cigarettes is AUD1.27816 per stick, or AUD1,893.57 per kilogram of tobacco content where tobacco is not in the form of a ‘stick’ or is in a stick that exceeds 0.8 grams in weight.[1] This paper builds on the concept that such a large excise tax liability can provide significant profits if that tax is evaded.

The Black Economy Taskforce, appointed by the Australian Government, in a report provided in 2017 did, however, make a statement related somewhat to ‘profitability’ in a comparison with illicit narcotic drugs, although the methodology was not provided, nor the term ‘street price’ defined and was seemingly based on private submissions. Significantly, the observation is that profitability in ‘smuggling’ of tobacco is some four times higher than illicit drugs with a penalty if caught being only modest in comparison with the level of imprisonment given to those smuggling cocaine or heroin (Commonwealth Treasury, 2017, p. 306), stating:

We have been informed that cocaine with a street value of $2.3 million here will have a cost of about $150,000, with heroin being similarly priced. The penalty for smuggling both is imprisonment. Whereas smuggling tobacco costing $150,000, with a street value of $10 million here, would, under current sentencing practices, generally result in a modest fine.

2. Methodology

In terms of the most current estimates of the revenue loss (or tobacco excise tax gap) from the illicit trade in tobacco, the figure published by the Australian Taxation Office (ATO) for 2021/22 is AUD2.34 billion on a ‘net’ basis, or AUD5.2 billion on a ‘gross’ basis. In this case, the gross tax gap is the excise tax payable on all illicit tobacco entering Australia, and the net tax gap is the excise payable on the illicit tobacco that was not intercepted and seized by authorities. It is also important to note that Australia no longer has a domestic tobacco manufacturing sector, with the last tobacco growing being in 2006 and cigarette production ceasing in 2015 (Australian Taxation Office, 2024; Freeman, 2016), meaning that in this paper its methodology will be based upon imported cigarettes only.

The publication of both net and gross tobacco excise tax gaps will assist somewhat in examining the profitability of the illicit tobacco trade, as the loss of product by criminals upon its detection crossing the border or in the market is a ‘cost of doing business’ when considering profitability. This paper will use the ATO’s published figure from the tax gap, which shows that it ‘intercepts’ around 16 per cent of illicit tobacco, which will become a ‘cost’ to the criminal.

Before outlining a methodology, there are some parameters to confirm and assumptions to outline. While commonly measured as one gram of tobacco comprising a ‘stick’, this paper uses the Australian excise law measure of 0.8 grams comprising a cigarette stick.[2] There are 20 cigarettes sticks to a ‘pack’, 10 packs to a ‘carton’, and a ‘twenty-foot equivalent’ (TEU)[3] shipping container can ship 475,000 packs or 47,500 cartons (Tobacco Free Kids, 2008, p. 2).

The ‘Cost Insurance and Freight’ (CIF) value of cigarettes into Australia calculated with reference to the Comtrade database (United Nations, 2024) using Harmonized System Code 2402 for 2023 reports total CIF at USD312,986,435 and total net weight at 7,448,112 kilograms. Total CIF is then converted to AUD at the average rate of exchange for 2023 of 0.6645 for a total CIF in AUD of 471,010,436.[4]

To establish values for packs, cartons and shipping containers, the number of imported sticks into Australia for 2023 needs to be calculated, for which total CIF is divided by total net weight, which provides for a CIF of AUD63.24 per kilogram. To convert this to a cigarette stick of 0.8 grams, the AUD63.24 per kilogram CIF is further divided by 1,250 for a CIF price per stick of AUD0.051, which then equates to AUD1.02 per pack, AUD10.20 per carton and AUD484,500 per shipping container.

Of note at this point is that the current excise equivalent duty rate of AUD1.27816 per stick on this shipping container can be assessed, being 475,000 packs multiplied by 20 sticks per pack, multiplied by the current excise equivalent duty rate. The equation is significant at a total excise equivalent duty of AUD12,142,520 and will allow criminals to offer pricing significantly below that offered by the legal supply chain.

The first steps in proposing a methodology can now be developed, which look at the cost of acquiring a container of cigarettes and importing that container into Australia. Notwithstanding, that container will not be declared as cigarettes to authorities. The components of acquiring a TEU container of cigarettes and importing that container are set out in Table 1.

The second stage is then to look at the proceeds from the sale of the cigarettes ‘on the black market’ through channels such as the tobacconist retail outlets mentioned above as being targeted in criminal gang violence, or as internet-based sales. In terms of retail outlets, Bucci (2023) states that consumers can expect to pay half of the retail price of the same legal tax-paid product.

In terms of a legal retail ‘average’ per price pack, in August 2023 this sat at around AUD40, which is consistent with the published ‘recommended retail price’ for both British American Tobacco (BAT) Australia’s and Phillip Morris International (PMI) Australia’s leading brands of Winfield Original and Marlboro Red, at AUD42 per pack.[5]

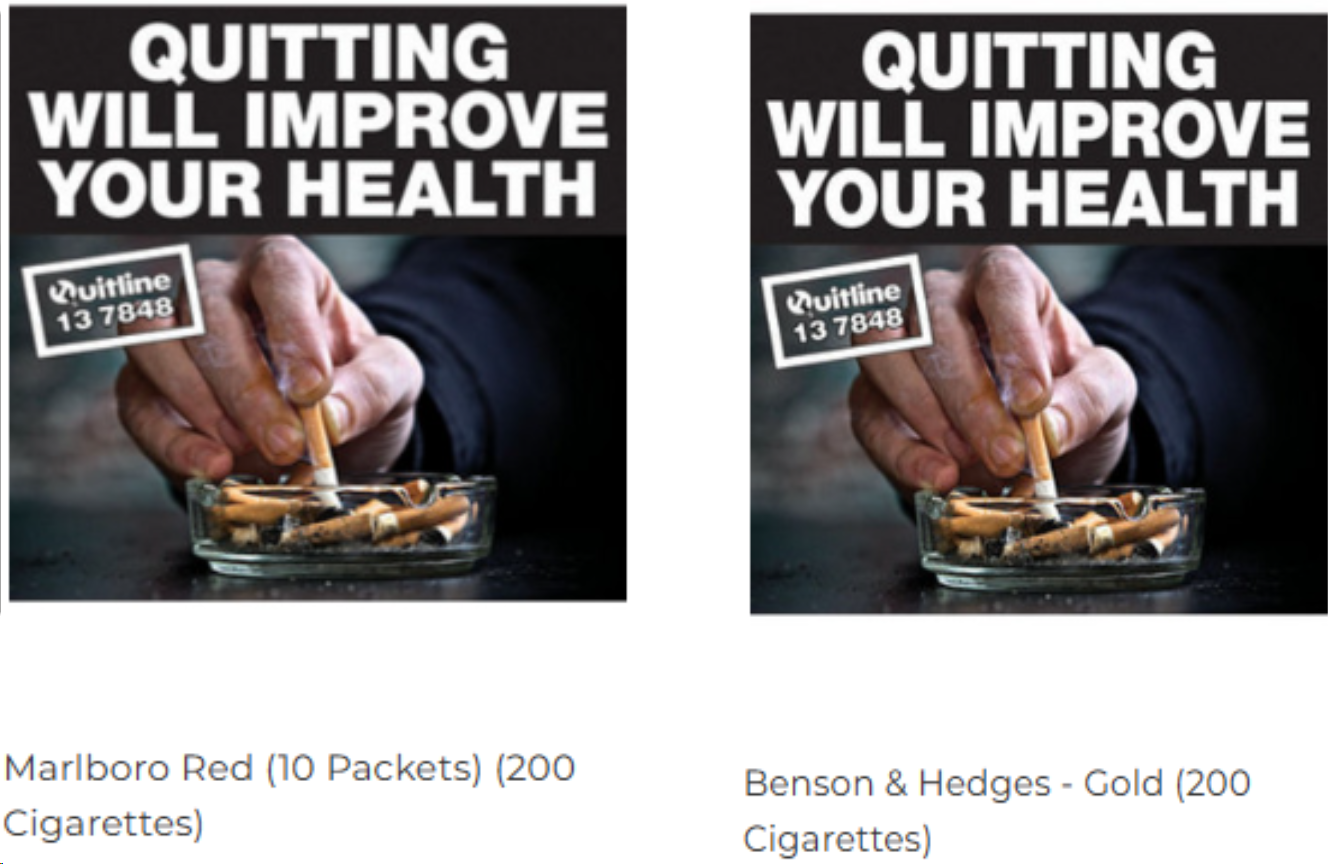

Online sales are also available and perhaps are a more immediate guide to the market price of illicit cigarettes. Figure 1 includes two products readily available online during the preparation of this paper with a simple search for ‘cheap cigarettes in Australia’ and in fact appears to indicate that illicit cigarettes may be for sale around or just below half the price of legal cigarettes – the only issue for consumers may be that they are required to purchase a carton at a time.

Figure 1 again includes popular brands offered by BAT Australia, ‘Benson & Hedges Gold’ and PMI Australia, ‘Marlboro Red’, both packs of 20 in a carton of 10 packs, or 200 cigarettes. In these cases, this illicit pack sales price has been set at AUD18.50 and AUD19.50 per pack, respectively. This paper will use a simple average of these two leading brands of AUD19 per pack.

The potential profits from illicit cigarettes sales in Australia for one TEU cigarettes can then be estimated as shown in Table 2.

3. Discussion

If the estimation in Table 2 is accurate, it represents a 1,500% return on investment. At this level of potential profitability, a criminal would only need one container in 16 importations to be successfully smuggled across Australia’s border to make a profit. As such, there is certainly an argument to support the idea that criminals and organised crime in Australia would see the distribution of illicit tobacco products as a lucrative venture among any other illegal activities they may currently be engaged in.

While tobacco excise taxes are set as this level, there will be opportunity for criminals to offer heavily discounted cigarettes to consumers, a 50 per cent discount, and capture a large market that will deliver significant profits. Therefore, the investment in combating illicit tobacco by the government and relevant authorities will need to continue and build on the current levels of 16 per cent interceptions to reduce the current opportunities for profit in this activity.

See Australian Taxation Office (n.d.), indexed to Average Weekly Ordinary Times Earnings (AWOTE) from 1 March and 1 September each year.

See Excise Tariff Item 5.1 Schedule to the Excise Tariff Act 1921.

Twenty Foot Equivalent (TEU) Shipping Container with dimensions 20ft x 8ft x 8ft.

Exchange Rates.org see AUD to USD https://www.exchange-rates.org/exchange-rate-history/aud-usd-2023.

See BAT http://www.ctceastern.com/pdf/530ceed4d3574703b2a154a16292ba7d.pdf and PMI https://www.pmi.com/resources/docs/default-source/australia-market/illicit-tobacco-in-australia---2022-full-year-report.pdf?sfvrsn=93c497b6_2.