1. Introduction

Continuous developments in science and technology, particularly the new generation of information technology represented by big data, AI, mobile internet and cloud computing, are driving the expansion of the global digital economy. Digital transformation has entered a stage of development. With the deep integration of the digital and physical economy, enterprises’ production and operation methods, and import and export trade methods, rely increasingly on digital resources to enhance the integration and analysis of data. In the digital era, the use of new technologies to explore the value behind government regulatory data, corporate financial and operational data has attracted widespread attention from all sectors of society. The ubiquitous application of digital technology and an emphasis on data resources are also present in the customs management scenario. For example, China Customs is trying to promote the construction of ‘Smart Customs’ to realise the digitisation, automation and intelligence of customs clearance and management, and to create an all-inclusive and chain-wide supervision system.

Post-clearance audit, as the current internationally accepted follow-up supervision and enforcement after customs clearance and release, is mainly through the audit of non-physical forms of enterprises’ import and export documents, account books, financial statements and related information. This audit is designed to allow Customs to access the whole process of import and export activities, including production, distribution, sales and use, forming an organic combination of pre-, on-site and follow-up management of the regulatory system. Post-clearance audit can be seen as a comprehensive interdisciplinary method that integrates modern customs management and audit. Therefore, in the era of ‘leading by scientific and technological innovation, applying the latest technology and equipment to customs management, realising informationisation and intelligence of management means and management methods’ (General Administration of Customs of the People’s Republic of China, 2019), opening up and integrating enterprise data using big data theory, mobile internet technology, AI and other new technologies and concepts, we continue to develop new systems of customs inspection. Through these new technologies and concepts, customs inspection is redefined in technological terms, including process re-engineering, intelligent audit analysis, remote control, system upgrade, risk prevention and control and intelligent decision-making. Achieving a new way of inspection of intelligent decision-making — intelligent supervision — is the current trend in customs development. Robotic process automation and artificial intelligence (RPA + AI) are the key driving forces for intelligent data analysis of customs inspection risk, reshaping the process structure with technical content and promoting the upgrade of customs risk analysis and subsequent regulatory analysis.

RPA, which refers to configuring software-based robots to automate repetitive, routine business processes (Aguirre & Rodriguez, 2017), is an emerging approach that can be adopted in various domains, such as public accounting, auditing, banking and public administration (Leshob et al., 2018). Applying RPA technology in the accounting management systems of government administrative areas can not only ensure the timeliness and convenience of government accounting department operations but also reduce costs (Xu & Kong, 2022). Similarly, RPA technology is highly compatible with the digital transformation of tax administration in terms of digital concepts, application scenario and data empowerment, and has the practical effectiveness of optimising experience, improving efficiency, integrating and standardising management (Research Group of Shenzhen Longhua District Taxation Bureau et al., 2021). Based on RPA technology, Cheng et al. (2018) collected and analysed the financial data of enterprises from several perspectives, explored the optimisation and improvement measures of the multi-dimensional financial analysis report generation process and stated that the application of RPA technology was more comprehensive and scientific for analysing and predicting the financial operation of enterprises. For auditing in corporate practice, integrating RPA technology can upgrade the audit process by automating it to combine the audit process and cognition, thereby increasing innovation and achieving new developments with new information technologies (Gong, 2021).

The current theoretical-level research involves developing financial analysis and the application of intelligent methods for it. The application-level research mainly focuses on case studies of RPA and BI (Business Intelligence) in data analysis, while the application of RPA technology in the analysis of financial and regulatory network data is scarce. In view of this, this paper explores the possibility of introducing RPA in customs risk data analysis for post-clearance audit, builds a framework model, and discusses an R&D strategy for risk data analysis of customs inspection based on intelligent RPA technology.

2. Core idea of the audit risk data analysis robot for post-clearance based on RPA

2.1. Concept and main functions

RPA is a type of intelligent software that can simulate and enhance the interaction process between users and computer systems according to predefined business processing rules and operational behaviours and automatically complete a series of specific workflows and expected tasks, to effectively realise the integration of human and business information systems (Cheng, 2021; Cooper et al., 2019). A post-clearance audit risk data analysis robot is designed as an intelligent analysis program that relies on RPA technology and combines the automation of data analysis processes. It follows established rules and procedures and adopts RPA technology that simulates, enhances, and expands the interaction process between inspectors and computer systems to automate the collection, cleaning, analysis, and visualisation of enterprise financial data and trade data of import and export links. Thus, automatic risk data analysis reports are generated to assist customs inspection staff efficiently complete the analysis tasks with a high degree of standardisation, repetitiveness, and reduced workload.

The robot can realise a series of functions, such as data collection, recording, calculation, analysis and reporting, and replacing the traditional manual functions to realise the automation of the regulatory data analysis process. RPA technology can be implemented into the task processing of each of these operations, tracking the process steps in detail and in real time, and excels in completing many repetitive, clearly defined and fixed logical tasks. Powered by AI technology, the risk data analysis robot can automatically focus on the financial data and business logic of the connected supervised enterprises, precipitate data value through data analysis, form data analysis services and provide analytical support for customs supervision scenarios. This can not only solve the problems of complicated financial and customs clearance data, time-consuming and laborious manual data analysis foundation work and the inability to extract values from data accurately and in a timely manner, but also promote customs business departments to better realise intelligent auditing, reshape process architecture, and improve the quality and efficiency of enterprise risk data analysis work.

2.2. Legal and technical foundations

Although the application of RPA into post-clearance risk data analysis scenarios can add value in terms of efficiency, quality and cost savings, the technical and legal aspects in achieving such functions also need to be seriously considered. For example, according to customs law in China:

The post-clearance audit department may verify the accounts, documents and other relevant information of enterprises and units directly related to import and export goods and the relevant import and export goods to supervise the authenticity and legality of their import and export activities within three years from the date of release of import and export goods or within the period of customs supervision of bonded goods or duty-free imported goods and within three years thereafter…(State Council of the People’s Republic of China, 2016, item 1)

This provides support to acquire data for risk data analysis at the jurisprudential level. In addition, in terms of business data acquisition techniques, data provided from enterprises to China’s customs currently is fully to realise the unit consumption data exploration case presented in this paper.

2.3. Practical value

Implementing the post-clearance audit risk data analysis robot can bring value to the full implementation of follow-up supervision by customs, which can be measured by efficiency, quality, cost savings and value added. In terms of efficiency, the robot can largely imitate manual operations; complete simple and repetitive operations, such as data entry and data calculation, and speed up data processing and analysis. In terms of analysis quality, the robot can avoid various low-level errors made by inspection and enforcement officers, and its operation is based on preset rules, which eliminate the variability of output to a certain extent and provide a high degree of standardisation. Regarding cost savings, the robot can achieve unified management of multi-process automation tasks, reducing labour costs. As for adding value, the application of robots promotes changes in the organisational structure of customs supervision, the intelligent transformation and upgrading of customs, and the optimisation of the human resource management of the post-clearance audit team.

3. Construction of the robot model

3.1. Theoretical framework

The post-clearance audit risk data analysis robot is an application of RPA in the field of inspection risk data analysis involving collaboration between customs and enterprises. The development strategy of the customs inspection risk data analysis robot includes five stages: determining the analysis theme, clarifying the analysis content and ideas, automating data collection and processing, automating data analysis and presentation, and automating data analysis reports.

The analysis theme refers to the established analysis objective of the risk data analysis robot and determining the analysis theme should clarify the application scenario and analysis purpose. Application scenario refers to the scenario of the risk data analysis theme, including clearance data, financial, and industry data and the problems existing currently, and should be centred on solving the pain points of the scenario. The analysis purpose is centred on solving the problem. Establishing the analysis purpose determines the analysis value of the risk data analysis robot. Before beginning the risk data analysis, it is necessary to categorise the analysed data, determine why the data analysis should be implemented, and what should be solved through the analysis. Moreover, whether the purpose of the analysis is to understand the current situation, its causes, or predictions need to be clarified. To evaluate the current situation, the analysis process should focus on cleaning, summarising and refining the data; to analyse the causes, the reasons behind the phenomenon need to be examined; to conduct predictive analysis, the accuracy of historical data and prediction methods also need to be considered.

After clarifying the purpose of the analysis, we need to determine the content and ideas of the analysis and build an analytical framework. Analysis methods, such as parametric analysis, comparative analysis, structural ratio analysis and cross analysis, are commonly used. According to the different analysis requirements and data characteristics, the choice of analytical methods has a significant impact on the effectiveness of risk data analysis. Based on the analysis method, the analysis purpose is deconstructed into several different points, and the entry point of the analysis is clarified and then refined for the specific content. For example, the parametric analysis method enables comparative analysis of standardised parameters, while the structural analysis method looks at the ‘cross-section’ of the data and explore its relative relationships. To analyse the data from the enterprise side, we need to focus on data calculations and the entire process of import and export, to promote customs supervision. The content framework of the post-clearance audit risk data analysis robot is divided into two parts: standardised data analysis by enterprises and customs risk discriminant analysis, which includes parameter, trend, structural ratio and ratio-compared analyses. Customs risk discrimination analysis includes industry, customs clearance data and security control category analyses. Each analysis is clear and constitutes the content architecture of the post-clearance audit risk data analysis robot, as shown in Figure 1.

3.2. Model construction

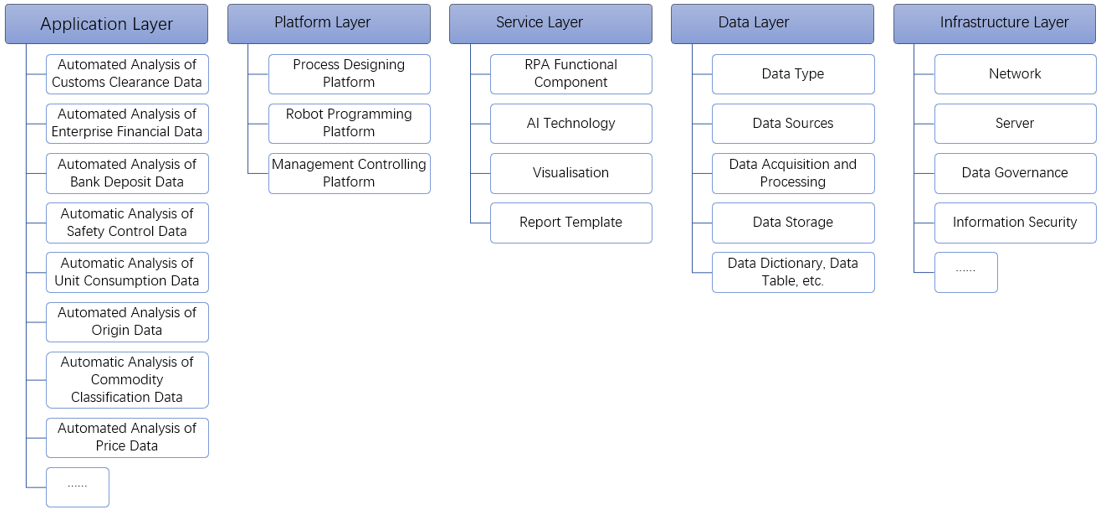

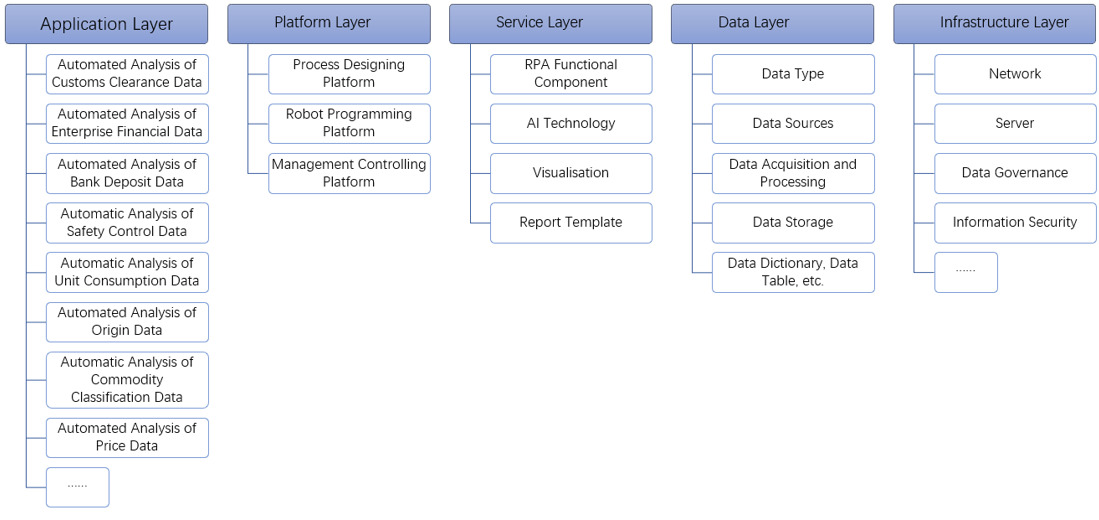

The risk data analysis robot model for post-clearance audit is constructed as a guide for intelligent data analysis that clarifies the construction goals of the robot and its specific applications. The model also discusses the data processing mechanism and visualisation generation mechanism of RPA technology, to guarantee the feasibility, rationality and compliance of the system’s implementation. Risk data analysis is essentially a process of data collection, screening, calculation and analysis. Based on the characteristics and advantages of RPA + AI technology in processing, rapid deployment and multi-terminal compatibility, this study constructs the framework model of the customs inspection risk data analysis robot. The framework model specifically includes different layers of infrastructure, data, service, platform and application, as shown in Figure 2.

The infrastructure layer is the foundation of the data, service, platform and application layers, providing basic services for each layer, including servers, networks, storage, data governance and information security, which guarantees the security of the operating environment for the risk data analysis robot. The data layer is the foundation of the data for the post-clearance audit risk data analysis robot, including the original enterprise financial, trade and customs clearance data, the mechanism of data collection and processing, and the formation of data storage, data dictionaries, data tables and other documents. The original enterprise and customs data are structured, semi-structured and unstructured data with various sources, including data of various information systems supervised by enterprises and customs, files and electronic documents. The service layer provides RPA functional components, AI technology, visualisation services and data analysis reporting services for the customs audit risk data analysis robot. The platform layer includes three parts: the process design platform, robot program and management control platform. This layer is mainly responsible for designing risk data analysis robots. The application layer is a specific application of RPA and AI technology in the field of post-clearance audit risk data analysis and is a specific application scenario for robots to realise automation, which consists of an organic combination of analysis robot clusters. In the work of audit risk data analysis, this layer can realise the automated analysis of enterprise customs clearance data, industry average data and enterprise bank deposit data.

4. An exploratory case study: unit consumption data analysis robot

This study presents an exploratory case of the analysis of unusual unit consumption data in processing bonded trade verification risk monitoring.

4.1. Analysis theme

Unit consumption verification plays an important role in the bonded trade audit of Chinese customs. Unit consumption refers to bonded trade enterprises, in normal production conditions, processing production units of finished products exported (including deep processing of finished products and semi-finished products) consumed by the number of imported bonded materials. Unit consumption includes net consumption and process losses. The principle of unit consumption supervision is ‘enterprise truthfully declared’, that is, the processing trade enterprises must report unit consumption records to Customs. At present, problems in the bonded supervision of unit consumption management focus on the use of early recorded unit consumption, fuzzy declaration, concealment of interception, and other methods of overstatement or understatement of bonded materials unit consumption. Therefore, in the process of post-clearance audit, attention should be paid to the processing trade enterprises to perform reasonable control and analysis of unit consumption. The first step is to analyse the rise and fall of unit consumption in each period using cost statements and compare it with consumption quota, determine the period that deviates from the consumption quota to a great extent, review the cost calculation account in this period, then determine unusual consumption, trace it back to the material receipt according to the voucher number of this matter, and examine whether there is any misrepresentation on the material receipt. This enables effective management of the production and operation activities of the processing trade enterprises and provides recommendations for bonded supervision.

4.2. Analysis contents and methods

After defining the theme of unit consumption data analysis, the specific related content is determined according to the analysis logic and methods. The analytical methods used include parameter comparison, structural ratio analysis and balance analysis. Combined with the needs of customs supervision from the Chinese government, the unit consumption data analysis robot is divided into standardised data analysis for enterprises and customs risk discrimination analysis, where the standardised data analysis includes standard parameter, structural ratio and balance analyses. Customs risk discriminant analysis includes industry, overall trend, ratio-compared and digital empowerment analyses. For example, structural ratio analysis is a credibility analysis, performed by calculating the reasonable degree of the composition ratio of raw material consumption, finished product output, defective products and scrap. To determine the credibility of the consumption of an enterprise’s customs declaration, the balancing analysis method helps to calculate the relevant items in accordance with the accounting standards and bookkeeping principles, as well as the intrinsic dependence between economic activities. Risk discrimination analysis uses the industry average, the overall production technology trend of enterprises and a comparison year-on-year to determine whether the unit consumption declaration is unusual. This includes, for example, whether there is a long-term unchanged or higher than industry average, if the unit consumption adjustment change rate is large, or the declared loss rate is high.

4.3. Automated data acquisition and processing

The post-clearance audit risk data analysis robot accesses networked enterprise data files to extract and store serial ledger information, but the raw data collected often has duplicate values, empty rows, empty columns and abnormal values. These illogical relationships can cause a reduction in data quality and need to be further examined. The data can be organised in various ways, and the subsequent statistics and analyses are performed on the premise of standard formats; therefore, the data needs to be standardised. The accuracy and completeness of the acquired data are checked and analysed by converting data types, removing duplicate information, identifying abnormal data and identifying early warning signs to ensure the quality of data analysis. The robot screens the keywords involved in unit consumption and extracts the corresponding analysis data according to preset rules, completes the automatic screening work, saves the data to the data centre and narrows the scope of data for additional processing and analysis.

4.4. Automated data analysis and visualisation

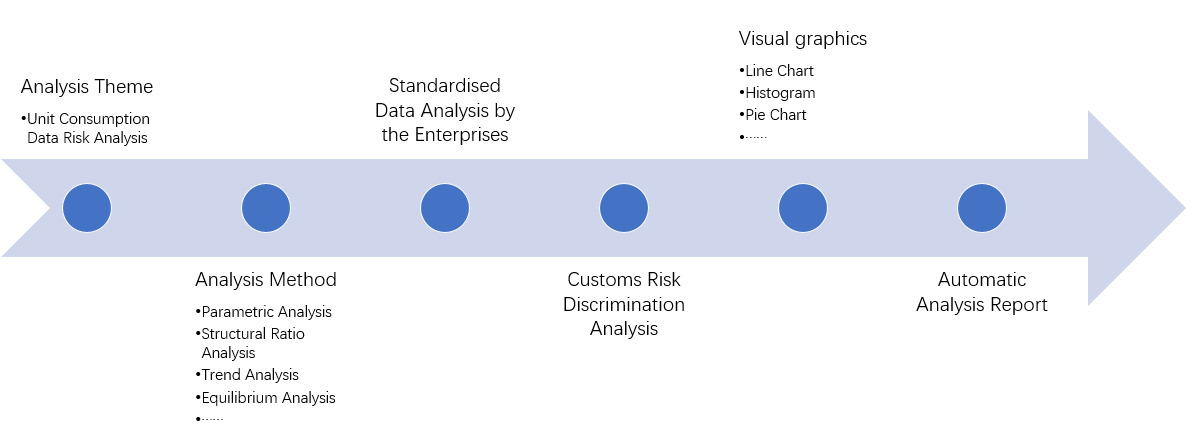

This phase of automated data analysis focuses on defining the unit consumption data analysis process and automating the analysis using intelligent RPA technology. The analysis process includes the analysis theme and methods to be applied, the specific content of the standardised data analysis from enterprises and customs risk discrimination analysis and explores the type of visual graphics for representation. The post-clearance audit risk data analysis robot optimises the specific process of the analysis model, sets logical analysis rules according to the focus of the task, calculates data and completes the corresponding data analysis by means of data tables, arrays and dictionary-related activities, and algorithms, such as loops and traversals. For example, trend analysis of unit consumption provides an analysis of the overall situation of unit consumption, such that customs officers can understand the status of the enterprise’s unit consumption. The visualisation graph is in the form of a line graph to allow clear and intuitive understanding of the unit consumption’s trend. The flow of unit consumption data analysis is shown in Figure 3.

At the automated data presentation stage, the data analysis visualisation template is predefined according to the analysis theme, and different visualisation graphics are selected for different analysis contents. The post-clearance audit data analysis robot inputs the data analysis results into a Microsoft Excel analysis template in the running process to realise data presentation automation. For example, a line graph can be chosen for trend analysis to show its data direction because it connects individual data points and can simply and clearly show the trend of data changes; in structural ratio analysis, a pie chart can be chosen to present the enterprise in the processing trade under the composition of raw material consumption, finished product output, defective products, scrap and other ratios. This allows information to be conveyed more clearly and intuitively.

4.5. Automated report

When conducting a post-clearance audit risk data analysis, it is often necessary to write an analysis report to present the results, making it easier for the users to understand. The post-clearance audit risk data analysis report presents the current situation of the enterprise under audit, the problems and their causes and conclusions of the specific analysis project. The automated report is a key method that helps customs officers understand the current situation of the enterprise’s operation and problems, grasp the information and use it for decision-making. The automation stage of the data analysis report is essential, and the analysis report template file needs to be developed before the specific application is carried out. For example, in the unit consumption risk data analysis, the report structure is divided into title page, table of contents, summary and body. The title page should be concise and straightforward to indicate the content of the analysis report. The table of contents is a tool to reveal the analysis report and help inspectors understand the main content of the risk data analysis report. The summary is an excerpt of the important analysis points and includes basic elements, such as background, purpose, ideas and conclusions, specifically the main objective and scope of the risk data analysis work, results and important conclusions. The main body is the core part of the risk data analysis report, which systematically and comprehensively expresses the process and results of the data analysis. This main text of the analysis report is divided into four parts: background and purpose, ideas, content, conclusions and recommendations.

For example, the unit consumption data analysis robot can set different analysis rules according to different analysis contents. When it starts to analyse standard parameters, it can set a reasonable range of differences, analyse the abnormal fluctuations that deviate from the standard unit consumption parameters, focus on the unit consumption data with unreasonable fluctuation ranges and analyse specific risk factors in a targeted manner.

4.6. Further discussions on the case study

In this exploratory case study, we focused on the technical implementation path of the robot. Here we will further discuss the data collection and risk prevention issues that need attention when using the robot. One of the core issues to the proper operation of the case robot is the integration of the customs data information platform (e.g. customs declarations, unit consumption declarations, etc.) with the financial data of the enterprise. The robot is required to access the electronic networking data of the processing trade enterprises in the customs data information platform as well as the enterprise financial data collected through the enterprise financial data to match and integrate. There may be certain data fraud risks as well as machine discriminatory risks in this process. At present, in view of the relevant risks, the General Administration of Customs of the People’s Republic of China has issued ‘Customs big data resources sharing management rules’, and some relevant management measures, while the post-clearance audit department has also recently proposed to rely on Cloud Engine, GBase,[1] and other systems to bring together internal and external information to strengthen risk prevention through the ‘system + technology’ approach.

5. Conclusions

Traditional risk data analysis methods and technologies can no longer efficiently match the digital era in which customs operates, and customs management needs to introduce emerging technological tools and intelligent automated thinking to meet current challenges. The application of RPA technology in risk data analysis provides a good environment for collaborative regulatory data to empower enforcement management. Post-clearance audit risk data analysis is not only limited to enterprise data analysis but is increasingly integrated with national gate security and trade security to provide standardised and visualised data analysis for data demanders. Furthermore, it can also be extended to provide relevant suggestions for the development and management decisions of external customs business departments (e.g. taxation departments, business administration departments, etc.).

Based on RPA technology, this study constructs a robot framework model for customs post-clearance audit risk data analysis considering five levels: infrastructure, data, service, platform and application layers. The case exploration of the post-clearance audit risk analysis robot is elaborated in five steps: determining the analysis theme, specifying the analysis content and methods, automating data collection and processing, automating data analysis and visualisation and automating the data analysis report. The unit consumption data analysis robot is used as an example to explore the application implementation process and provides a useful exploration and feasible path for the automated processing of customs supervision risk analysis.

Cloud engine is the big data searching engine designed by China Customs to search and analysis data on trade. GBase is a Chinese self-branded database product launched by Nanda General Data Technology Co.